In the past few weeks, two stories caught my attention. One decried the growing wealth gap between the young and old in America. The other highlighted the growing difference between older and younger Americans on issues such as social values and morality.

Should we be surprised by either of these stories?

I think not.

Let’s look at the wealth gap first. I will get to the Social Values and Morality Gap in Part 2.

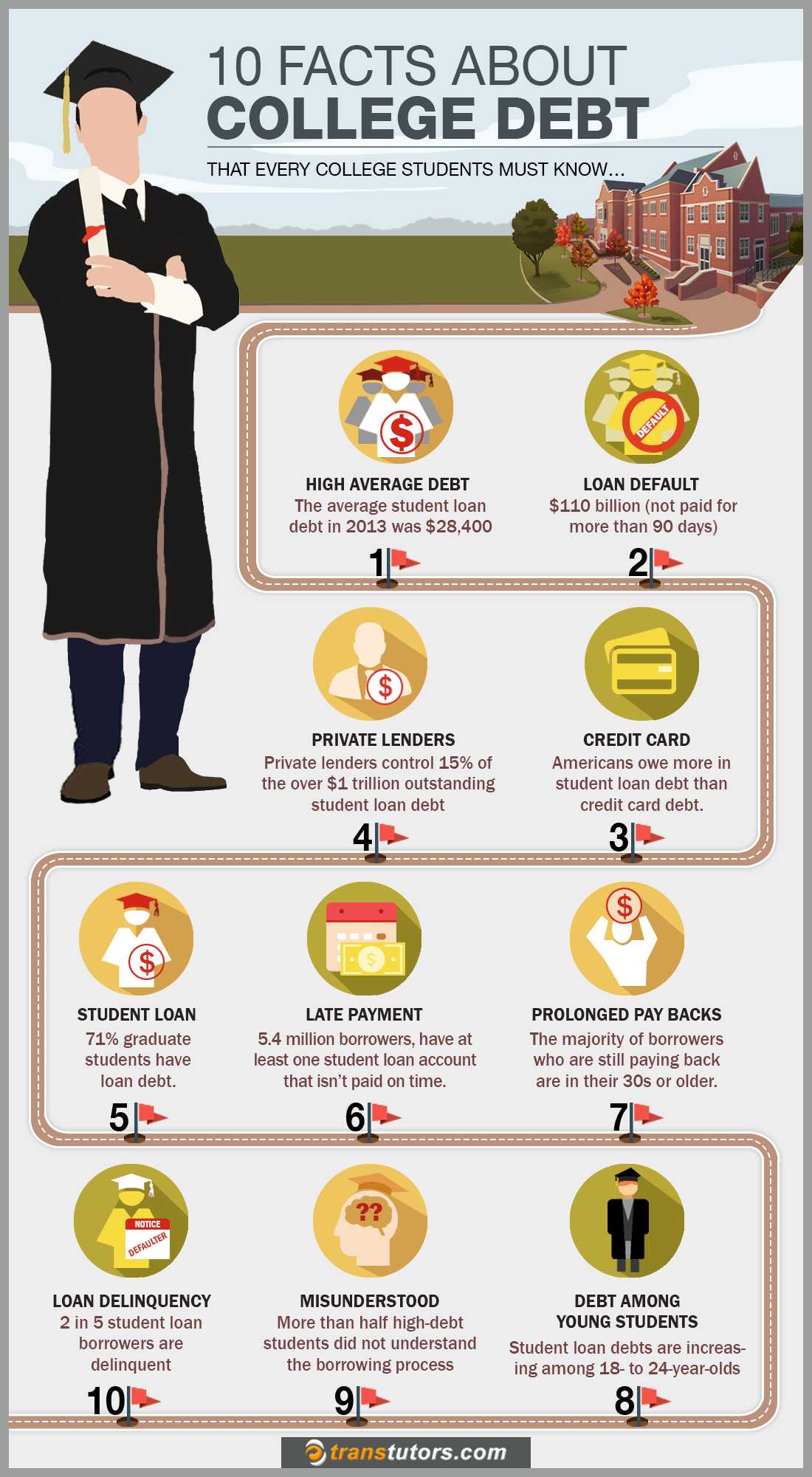

A report issued by the U.S. Census Bureau said the wealth gap between younger and older Americans has increased to the widest on record, worsened by a prolonged economic downturn that has wiped out job opportunities for young adults and saddled them with housing, credit card, and college debt.

The typical U.S. household headed by a person age 65 or older has a net worth 47 times greater than a household headed by someone under 35, the report said, adding that the gap in wealth is now more than double what it was in 2005 and nearly five times the 10-to-1 disparity a quarter-century ago, after adjusting for inflation.

Why is this? Part of it is caused by the economic downturn, which has hit young adults particularly hard. As I saw when I was a Dean at the University of Illinois, more young people are pursuing college or advanced degrees, taking on debt as they wait for the job market to recover. Others are struggling to pay mortgage costs on homes now worth less than when they were bought in the housing boom.

But that is not the whole story. All of us have gone through hard times at one point or another. I can recall when mortgage interest rates were 19 percent and buying a house was simply out of the question. I can recall unemployment rates running between 7 and 9 percent and double-digit inflation–none of which made life much fun.

Perhaps it’s the way many in the so-called silent and baby-boomer generations lived and spent money. Without sounding like some old geezer, I should point out that when I was in my 20s, I didn’t have a credit card. I did have a gasoline charge card from Standard Oil, but the thought of charging meals, groceries, vacations, car repairs, etc. on a credit card was simply not an option. Credit cards were simply not the ubiquitous snares that they are today.

I paid cash for just about everything. I even paid back my student loan–though I was fortunate to have a large part of my college education paid for via the GI Bill.

Today, young people are crushed under the weight of credit card debt. Why? Because for many the thought of actually saving up to buy something is simply anathema. We are in the era of instant gratification. A lot of young people want things, and they want them now! So what do they do? They pull out those credit cards that aren’t already maxed out and continue to accumulate more debt.

And what about those houses that are now worth less than the mortgages? Why would a couple in their late 20s or early 30s opt to buy a $600,000 or $700,000 house with 5% down, an adjustable-rate mortgage, a balloon second mortgage and monthly payments of $5,000 or $6,000?

Why? Because they just HAD to have THAT house–even though common sense told them that home prices during the so-called “housing boom” were grossly over-inflated.

Call me old-fashioned, but I can guarantee you that there is no way I would have done that when I was starting out. That is what a lot of those Gen X-ers and Gen Y-ers did. And now many are suffering because of the choices they made.

The Census Bureau report comes just before the Nov. 23 deadline for a special congressional committee to propose $1.2 trillion in budget cuts over ten years.

But more importantly, it has created questions about the government safety net that has sustained older Americans on Social Security and Medicare amid cuts to education and other programs, including cash assistance for low-income families.

“It makes us wonder whether the extraordinary amount of resources we spend on retirees and their health care should be at least partially reallocated to those who are hurting worse than them,” said Harry Holzer, a labor economist and public policy professor at Georgetown University who called the magnitude of the wealth gap “striking.”

Wait a minute! The money that retirees are getting from Social Security and Medicare is money that they paid into the system all their working lives. Are they supposed to feel guilty about that? Older Americans paid into a system that was set up to supplement savings and private sector retirement plans such as profit sharing, employee stock ownership schemes, and savings incentive plans.

Social Security and Medicare are NOT entitlement programs. They are NOT welfare plans for retirees. In fact, the money retirees take out of Social Security and Medicare is in essence money they have loaned the federal government. That the federal government spent that money unwisely or delved into it to fund other programs is not the fault of those who made good faith payments into the system.

There is no doubt that the numbers contained in the Census Bureau report are striking. For example, the median net worth of households headed by someone 65 or older is $170,494. That is 42 percent more than in 1984 when the Census Bureau first began measuring wealth broken down by age.

The median net worth for the younger-age households was $3,662, down by 68 percent from a quarter-century ago, according to the analysis by the Pew Research Center. In all, 37 percent of younger-age households have a net worth of zero or less, nearly double the share in 1984. But among households headed by a person 65 or older, the percentage in that category has been largely unchanged at 8 percent.

Net worth includes the value of a person’s home, possessions and savings accumulated over the years, including stocks, bank accounts, real estate, cars, boats or other property, minus any debt such as mortgages, college loans, and credit card bills. Older Americans tend to hold more net worth because they are more likely to have paid off their mortgages and built up more savings from salary, stocks and other investments over time. The median is the midpoint, and thus refers to a typical household.

Households headed by someone under age 35 saw their median net worth reduced by 27 percent in 2014 as a result of unsecured liabilities, mostly a combination of credit card debt, mortgages and student loans. No other age group had anywhere near that level of unsecured liability acting as a drag on net worth. The next closest was the 35-44 age group, at 10 percent.

Among the older-age households, the share of households worth at least $250,000 rose to 20 percent from 8 percent in 1984.

It is highly irritating and unfair to blame retirees for the plight of the younger generation. Unless of course, those retirees didn’t do their job in rearing fiscally responsible offspring or, even worse, encouraged them to pile up credit card debt by promising them that a parental bail out was in the offing.

Retirees worked long and hard for whatever wealth they have managed to accumulate. And, as the Census Bureau report shows, most are NOT wealthy–not when only 20 percent have a median household net worth of $250,000 or more.

Most older Americans are working longer than their parents did. Both my parents were able to retire at 62. How many older Americans can do that today? Not many. In fact, most are working well into their late 60s and early 70s.

Indeed, the whole concept of “retirement” has transformed today. The notion of spending the alleged “Golden Years,” sitting on the front porch in a rocking chair watching squirrels and listening to birds, is simply hooey.

So when economists lament the fact that retirees have 47-times more household net worth than Generation X-ers or Generation Y-ers, I can’t help but to parapharase that old Smith Barney TV commercial that said: “They made money the old-fashioned way. They earned it.”

Amen to that.

(NEXT: When Does a Gap Become a Canyon? (Part 2)

Three and a half decades of service (and hazardous-duty pay) in hellholes—alphabetically, albeit not chronologically, Afghanistan through Zimbabwe—allowed me to accumulate a decent retirement nest egg. Having paid out of my life savings for my progeny’s university costs, I find myself irritated by politicians promising to cancel student debt. That means those of us who were responsible and already paid once would have to pay again for unknown and ungrateful recipients (many of whom squandered both the funds and their time by “studying” completely useless majors). Call me an old fogey, but don’t raid my life savings. I’m too old for Nam redux.

Amen, brother!